Are you thinking about buying a house in Guelph but wondering, “Can I even afford it with my income?” If you’re a first-time buyer, this question is likely top of mind.

In this post, we’ll break down how much house you can afford based on different income levels, what types of properties are within reach, and the key steps to boost your buying power. Whether you’re just starting out or aiming for a bigger home, this guide will help you set realistic expectations and create a smart plan.

Do you want a seamless and straightforward home buying process? One of our detailed buying guides can help!

Step 1: Understand the Mortgage Basics

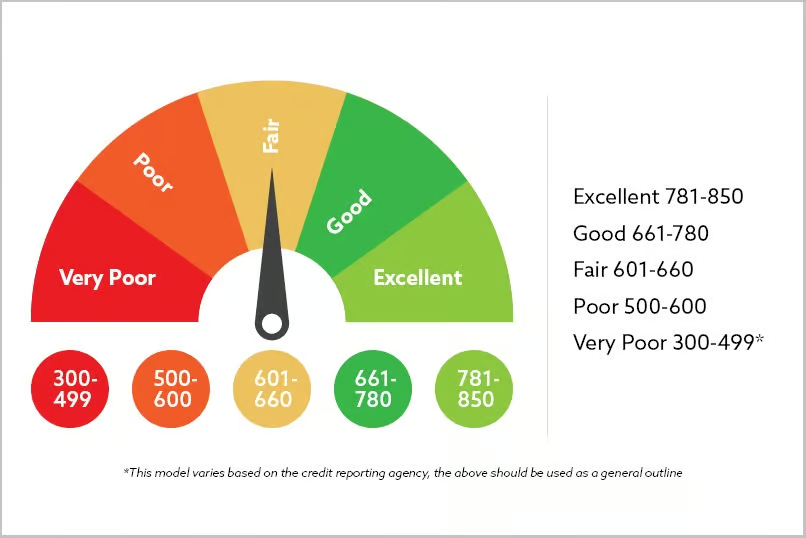

Credit Score – The First Hurdle

Your credit score is one of the first things lenders look at. While you don’t need a perfect score, aiming for 700+ will give you access to better rates and terms.

- Above 700: You’ll have more lender options and lower interest rates.

- Below 700: You can still get a mortgage, but things get trickier under 650.

- No Credit History: This is actually worse than low credit. Start building credit as soon as possible—banks want to see that you can manage debt responsibly.

Debt Service Ratios (GDS & TDS)

Lenders also analyze how much of your income goes toward housing and other debts:

- GDS (Gross Debt Service): The cost of owning the home (mortgage, property taxes, and utilities) should be under 39% of your gross income.

- TDS (Total Debt Service): Your housing costs plus all other debts (car loans, student loans, credit cards) should be under 44% of your gross income.

📘 Example Calculation TDS:

- Gross income: $120,000/year → $10,000/month

- Housing costs (GDS): $2,800/month

- Car loan: $450/month

- Student loan: $250/month

✔️ This is well within the 44% TDS threshold.

Before going any further, you may be asking, “why buy my house in Guelph?” The posts below might inspire you to start packing:

- Start Your Pre-Approval Today

- Is Guelph, Ontario, a Good Place to Live?

- 5 Reasons to Make Guelph Your Next Home

- Guelph Vs Toronto: Is It Time to Move?

What You Can Afford in Guelph Based on Income

Let’s assume:

- Interest Rate: 3.99%

- Amortization: 30 years

- Credit Score: 700+

- No other debts

1. Single Buyer – $70,000 Income

- Max Purchase Price: $350,000 (with ~$30,000 down payment + closing costs)

- Monthly Mortgage Payment: ~ $1,583

- What You Can Get:

- Smaller condos in Guelph, typically 1-bedroom units.

Example: A 1-bed, 1-bath condo at 53 Conroy recently sold for $310,000 with $380/month condo fees.

This affordable 1-bedroom, 1-bathroom condo in Guelph’s desirable Old University area offers an open-concept layout, updated 4-pc bath, and carpet-free living. Just minutes from the University of Guelph, shopping, and major highways, it’s perfect for first-time buyers, downsizers, or investors. Click here for more info!

Tip: If you want more options, look at Cambridge or Kitchener-Waterloo, where sub-$350K properties are more common. Click here to see listing under $350,000 in Guelph, KW & Cambridge!

2. Couple – $120,000 Combined Income

- Max Purchase Price: $600,000 (with ~$50,000 down payment)

- Monthly Mortgage Payment: ~ $2,712

- What You Can Get:

- Larger 2-bed condos or condo townhouses.

- Possibly a small detached home in certain areas

Example: A 3-bed, 1-bath detached home on Edinburgh Rd N sold for $549,900. Recently updated & 60 x 100 ft lot. Click here for more info!

Click here to view other properties in this price range!

3. Couple – $200,000 Combined Income

- Max Purchase Price: $1,000,000 (with ~$75,000 down payment)

- Monthly Mortgage Payment: ~ $4,577

- What You Can Get:

- Luxury townhomes or large detached homes.

Example: A 4-bed, 4-bath home with an in-law suite in Guelph’s west end sold for $915,000. Click here to view this property.

Click here to see more homes in this price range!

Looking for even more advice before buying your next property? The posts below can help you check off all the boxes:

- Title Insurance in Canada: What It Is, Why It Matters & How We’ve Got You Covered

- How Much Does It Cost to Buy a House

- Checklist for Buying a Home

5 Ways to Afford More Home in Guelph

If these price points feel limiting, here are 5 proven strategies to boost your buying power:

- Add a Co-Signer: A parent or family member can help you qualify for a larger mortgage.

- Increase Your Down Payment: Save more or receive a gift from family.

- Buy a Home with a Legal Basement Apartment: Rental income can offset mortgage costs.

- Example: A 3+2 bedroom home on Normandy sold for $850,000 and the basement alone could rent for $2,000/month.

- House Hack: Live in the basement apartment and rent out the upper floor.

- Focus on Credit & Debt: Raise your credit score above 700 and pay off high-interest debts to increase approval amounts.

Nearby Towns with Better Value

If Guelph prices are stretching your budget, consider these nearby markets:

- Fergus/Elora: Avg. price around $650,000 (25 mins from Guelph).

- Palmerston & Minto: Avg. price around $550,000 (50 mins from Guelph).

- Example: New-build 4-bed townhomes with legal basement apartments are selling for $639,000—the basement alone could cover $300,000 of your mortgage with rental income.

- Cambridge: Lots of freehold options under $700,000 and closer to the 401.

Getting into the housing market doesn’t mean buying your forever home right away. It’s better to start small and benefit from market appreciation than to wait while prices outpace your savings.

If you want a personalized breakdown of what you can afford to buy in Guelph, reach out to our trusted mortgage partner, or contact the GoWylde Real Estate team. We’ll help you strategize and find the right home—whether in Guelph or beyond.

Our top Guelph real estate agents are here to answer all of your questions. Reach out today at info@gowylde.ca or call 519-826-7109 for more information.